IRAs… Yes, This Will Be On The Test

WE’LL GET THERE WHEN WE GET THERE… DON’T MAKE ME STOP OR SO HELP ME…

WOULDN’T IT BE NICE IF WE WERE OLDER?

THEN WE WOULDN’T HAVE TO WAIT SO LONG

AND WOULDN’T IT BE NICE TO LIVE TOGETHER

IN THE KIND OF WORLD WHERE WE BELONG?WOULDN’T IT BE NICE, BEACH BOYS

Financial security was probably not what The Beach Boys were singing about. But wouldn’t it be nice to have a few bucks of your own? A little independence? Isn’t that “the kind of world where we belong”? Maybe not completely relying on Social Security?

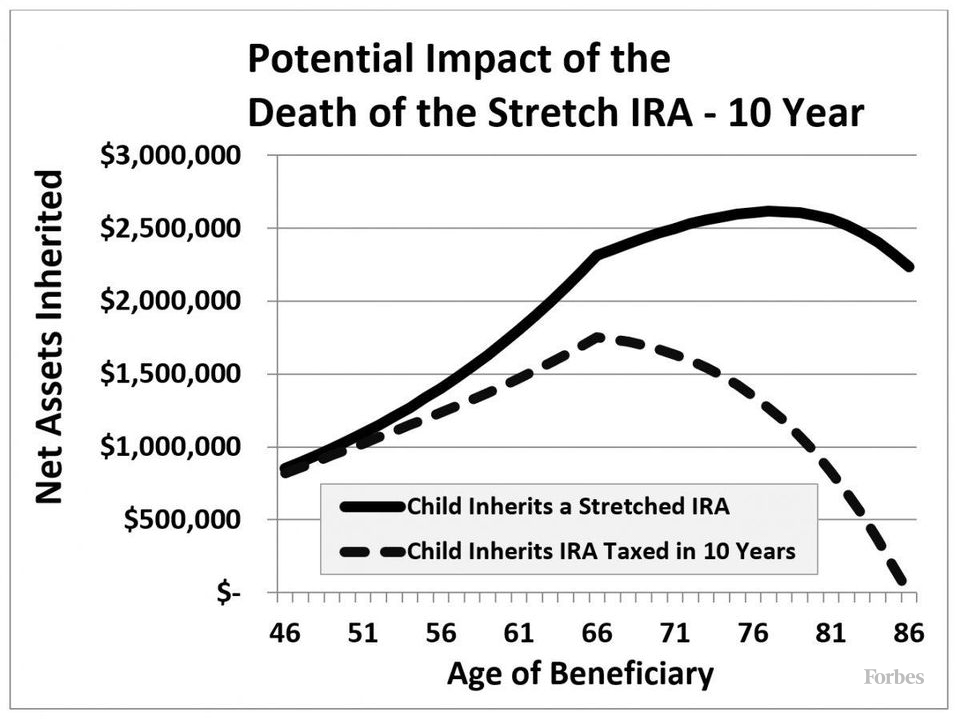

You choose from two types of Individual Retirement Account: Traditional or Roth. Traditional IRA, you deduct contributions when the money goes in and pay income tax on distributions when the money comes out. Roth IRA, you pay tax on contributions when the money goes in and do NOT pay income tax on distributions when the money comes out.

Concerned about skyrocketing income tax rates? Roth IRA for you! Want to dump more money into the account now and worry about taxes later? Traditional IRA at your service.

How to make it happen? Middle class workers and savers (that’s you) have been pumping money into tax-advantaged accounts since the 1980’s. How much? Nobody seems to know for sure. Probably somewhere between 30 and 40 trillion dollars. And even today, that’s real money. So how can you get into the game?

You Must Have Earned Income

Only folks with “earned income” get to contribute to an Individual Retirement Account. Did you get a W-2? Then you have earned income. For sure. No question. “Safe Harbor.” But nowadays, in this “gig economy” many folks are getting Form 1099s for earned income. Hello UBER drivers! Earned Income includes wages, salaries, commissions, self-employment income, taxable alimony. Earned Income does not include rent, royalties, annuity payments, pension, deferred comp.

How much can you contribute? All of your “earned income”… up to the contribution limit. For 2021 (no change from 2019 or 2020) the contribution limit is $6000, $7000 if you are 50 years old or more.

But If You Have Too Much Earned Income — No Roth For You!

You worked your butt off. Income tax biting hard. But you see even higher taxes on the horizon… Wouldn’t it be nice to dump some dough into a Roth and not worry about those higher taxes? Obviously. But you poor sap… if your income is over $124,000, your contribution is limited. And if you make more than $139,000, you are skunked! No Roth at all! Really? Nope…

Too Much Earned Income and Still Get the Roth? How Can This Be?

You put in the overtime. You worked a second job. You sold GRIT, greeting cards, and flower seeds door-to-door. Too much income! You cannot have a Roth! Or can you?

You paid the income tax. You are not eligible for a Traditional IRA income tax deduction. You are not eligible for a Roth. Now what?

Your income is “too high” for a Roth. (Hello doctors, nurses, foremen, engineers!) But you can still make contributions to a Traditional IRA. Taxable contributions. Contributions that are NOT tax deductible. How much can you contribute? Same as anyone else, see above. The difference is that you cannot take an income tax deduction for those contributions.

OK. So now you put the maximum leftover money into a Traditional IRA. “How does that help with the Roth?”, you ask. Good question. The answer is that you can convert a Traditional IRA that was established with taxed money into a Roth IRA. You can even convert untaxed IRA money into a Roth, if you pay the income tax. You can do this…whenever you want.

“Allowable conversions. You can withdraw

all or part ofthe assets from a traditional

IRA and reinvest them (within 60 days) in

a Roth IRA. The amount that you withdraw

and timely contribute (convert) to the Roth

IRA is called a conversion contribution.”

IRS Pub. 590-A, page 27.

To Sum It All Up: You cannot establish a Roth IRA because you have too much income. But you can still establish a Roth IRA anyhow, despite too much income, if you take this extra step.

I told you this stuff was nuts. Believe me now?

I Do Not Work Outside the Home, But I want to Retire Too… Can My Spouse Contribute to My IRA?

Yes! Even if you do not work for money outside the home, your spouse can contribute on your behalf. Yay domestic partnership! Wedded bliss!

Just like your working-for-money spouse, you can put $6000 per year into your own IRA. And beginning when you are 50 years old, you can put an additional $1000 per year into your IRA. Pretty great!

Beware: All the same rules for income, retirement plans, contribution limits and so on apply to you as to your working stiff spouse. Sauce for the goose, sauce for the gander. Same rules apply to both. Including that Traditional to Roth Conversion thing that nobody can believe actually works. But does!

Can I Get Deductions for My IRA Contributions? Elementary My Dear Watson! If This Stuff Were Easy, Everybody Would Do It

RULE #1 You can never deduct contributions to a Roth IRA. Remember, the whole point of a Roth is pay tax NOW so no tax LATER.

RULE #2 You can always deduct contributions to a Traditional IRA, no matter how much income. Within the $6000 + $1000 limits. Unless you or your spouse are covered by an “employer retirement plan.”

If your employer sponsors a retirement plan, your IRA contribution will be limited or eliminated by the “Deduction Phaseout.” Limited or Eliminated. Depends on how much income you have. Same deal, but different limits if your spouse’s employer has a retirement plan. It gets complicated.

So, pick yourself up a copy of IRS Publication 590-A, Contributions to IRAs, for today’s numbers. Only 60 pages long, IRS Pub. 590-A is riveting reading. And if 590-A does not put you to sleep, may I suggest IRS Publication 590-B, Distributions from IRAs. A real page-turner! Sixty-six pages, that is…

Wondering if you are covered by an employer plan? Your W-2 Form has a box for that. If it is checked, you are covered.

You cannot deduct, but still want to contribute to your traditional IRA? File IRS Form 8606 with your tax return to fess up!

Changes in Tax, Medicaid, Business and Other Laws Make Lifeplanning™ a Necessity for Any Middle-class Family to Succeed

You have built a significant and successful life and family.

Of course, your success comes from hard work and talent. But continued success depends on how quickly one can respond to life’s changes.

And, as I am sure you are keenly aware, circumstances are putting pressure on the entire American middle class, and middle-class seniors in particular. I am referring, of course, to the frustrating jumble of COVID laws and executive orders, along with the trillions of social spending draining Medicare and Social Security trust funds. Not to mention today’s financial turbulence.

First, the infamous executive orders that required nursing homes to admit vulnerable seniors with COVID. Only 16% of Americans are over age 65. Yet according to the Centers for Disease Control and Prevention, this small group suffered 78% of all COVID deaths. The number goes to 94% when people over age 50 are included.

Hyper-inflation is already back. You are already paying double at the gas pump. I shudder to think what your heating bill will look like this winter.

With Congress and the President shoveling money out the door, how will Social Security and Medicare survive? You already know that their priorities are not your priorities.

Hence the necessity to recognize these new realities – threats, even – and act accordingly, by increasing awareness, effectiveness, and avoiding nursing home poverty. You can live your best possible life and still be justly proud of the legacy you leave.

LifePlanning™, of course, cannot be the only solution to all this, but it is definitely an important part of it.

And let me emphasize one highly relevant fact.

Pressed by the need to get legal advice and documents quickly and cheaply, a few seniors (and their kids) have started using some of the free resources available on the Internet. This “shortcut” may all too easily result in great financial and medical losses to the detriment of your wealth and health.

Quite an unnecessary risk, given the availability and affordability of a comprehensive, cost-effective, personalized solution like LifePlanning™.

The benefits of this approach are so clear and overwhelming that thousands of families and hundreds of millions of lifesavings have already been protected.

Nevertheless, I doubt if anyone in your family will appreciate its value and implications better than you.

Nothing is more compelling than evidence. Go to the website: www.davidcarrierlaw.com. A quick review will take only a few minutes.

If you like what you see, call our LifePlan™ Hotline at 800-317-2812 or email me at david@davidcarrierlaw.com for an online or live Workshop. In a very short time indeed, you and your family can verify the claims I have made.

Success in life has always depended on knowledge. Those who are better informed, or informed before others win for themselves and their families. That is really the overwhelming reason why LifePlanning™ is not just important but, I believe, essential.